Carol Topp CPA Rental Property Records free printable template

Show details

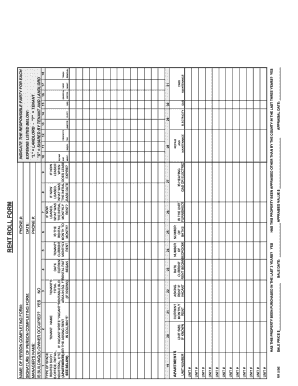

Rental Property Records Year Address of property Expenses Advertising Cleaning Purchase date Insurance Purchase Amount Legal fees Less value of land Maintenance Depreciated amount Tax prep fee Depreciation

pdfFiller is not affiliated with any government organization

Get, Create, Make and Sign rental income and expense worksheet pdf form

Edit your tax expense form for rental property form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your spreadsheet for rental property form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit rental property worksheet online

Here are the steps you need to follow to get started with our professional PDF editor:

1

Check your account. If you don't have a profile yet, click Start Free Trial and sign up for one.

2

Upload a file. Select Add New on your Dashboard and upload a file from your device or import it from the cloud, online, or internal mail. Then click Edit.

3

Edit rental income tax form. Rearrange and rotate pages, add and edit text, and use additional tools. To save changes and return to your Dashboard, click Done. The Documents tab allows you to merge, divide, lock, or unlock files.

4

Save your file. Choose it from the list of records. Then, shift the pointer to the right toolbar and select one of the several exporting methods: save it in multiple formats, download it as a PDF, email it, or save it to the cloud.

The use of pdfFiller makes dealing with documents straightforward. Now is the time to try it!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out carol topp cpa rental property records is a financial record associated with their rental properties form

How to fill out Carol Topp CPA Rental Property Records

01

Start by gathering all necessary documents related to your rental property, including income statements, expenses, and receipts.

02

Open the Carol Topp CPA Rental Property Records template.

03

In the designated sections, enter your property's address and other identifying information.

04

Record all rental income received, including dates and amounts.

05

Detail all expenses related to the property, such as maintenance, repairs, property management fees, and utilities.

06

Calculate your total income and total expenses to determine your net profit or loss.

07

Review the completed records for accuracy and ensure all supporting documentation is attached.

08

Save and back up your records for future reference or tax purposes.

Who needs Carol Topp CPA Rental Property Records?

01

Landlords managing rental properties who need to track their income and expenses.

02

Real estate investors looking to maintain accurate financial records for tax reporting.

03

Individuals preparing for tax season who want to ensure they have comprehensive documentation of their rental activities.

04

Property managers responsible for overseeing multiple rental units and their financial records.

Fill

rental property expense worksheet printable template

: Try Risk Free

People Also Ask about rental property record keeping template

Does rental income get reported to IRS?

All rental income must be reported on your tax return, and in general the associated expenses can be deducted from your rental income. If you are a cash basis taxpayer, you report rental income on your return for the year you receive it, regardless of when it was earned.

How does the IRS know if I have rental income?

Ways the IRS can find out about rental income include routing tax audits, real estate paperwork and public records, and information from a whistleblower. Investors who don't report rental income may be subject to accuracy-related penalties, civil fraud penalties, and possible criminal charges.

How do you calculate income and expenses of a rental property?

The 50% Rule states that normal operating expenses – excluding the mortgage payment – for a rental property can be estimated to be about one-half of the gross rental income. If the gross rental income is $1,000 per month then the estimated operating expenses could be $500 per month.

How does IRS find unreported income?

The IRS receives information from third parties, such as employers and financial institutions. Using an automated system, the Automated Underreporter (AUR) function compares the information reported by third parties to the information reported on your return to identify potential discrepancies.

How do you prepare a rental income statement?

What is included on a rental property income statement? Gross Rental Income should include: Operating Expenses. Net Operating Income. Monthly income expense statement. Year-to-date (YTD) Year-end. Trailing 12 months (T-12 statement) Cap rate.

How do I record income from rental property?

If you rent real estate such as buildings, rooms or apartments, you normally report your rental income and expenses on Form 1040 or 1040-SR, Schedule E, Part I. List your total income, expenses, and depreciation for each rental property on the appropriate line of Schedule E. See the Instructions for Form 4562 to figure

Our user reviews speak for themselves

Read more or give pdfFiller a try to experience the benefits for yourself

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I manage my expense spreadsheet for rental property directly from Gmail?

spreadsheet for rental property expenses and other documents can be changed, filled out, and signed right in your Gmail inbox. You can use pdfFiller's add-on to do this, as well as other things. When you go to Google Workspace, you can find pdfFiller for Gmail. You should use the time you spend dealing with your documents and eSignatures for more important things, like going to the gym or going to the dentist.

Where do I find spreadsheets for rental income and expenses?

It’s easy with pdfFiller, a comprehensive online solution for professional document management. Access our extensive library of online forms (over 25M fillable forms are available) and locate the rental income expenses spreadsheet in a matter of seconds. Open it right away and start customizing it using advanced editing features.

How do I make edits in rental property tax deductions worksheet pdf without leaving Chrome?

Get and add pdfFiller Google Chrome Extension to your browser to edit, fill out and eSign your rental property accounts spreadsheet, which you can open in the editor directly from a Google search page in just one click. Execute your fillable documents from any internet-connected device without leaving Chrome.

What is Carol Topp CPA Rental Property Records?

Carol Topp CPA Rental Property Records is a financial record-keeping system designed for landlords and property owners to track income and expenses associated with their rental properties.

Who is required to file Carol Topp CPA Rental Property Records?

Landlords and real estate investors who generate rental income from properties are required to file Carol Topp CPA Rental Property Records to ensure accurate reporting for tax purposes.

How to fill out Carol Topp CPA Rental Property Records?

To fill out Carol Topp CPA Rental Property Records, users must enter details such as rental income received, operating expenses incurred, property details, and any related deductions as specified in the provided forms.

What is the purpose of Carol Topp CPA Rental Property Records?

The purpose of Carol Topp CPA Rental Property Records is to help property owners organize their financial information, ensure compliance with tax regulations, and make it easier to prepare tax returns.

What information must be reported on Carol Topp CPA Rental Property Records?

The information that must be reported includes rental income, operating expenses, property management fees, repairs and maintenance costs, and any relevant deductions like mortgage interest or property taxes.

Fill out your Carol Topp CPA Rental Property Records online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Rental Income And Expense Worksheet is not the form you're looking for?Search for another form here.

Keywords relevant to landlord rental income and expense worksheet pdf

Related to printable rental income and expense worksheet

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.